Just over ten years ago, agency holding groups Publicis Groupe and Omnicom Group shocked the industry by announcing plans to combine their businesses in a “merger of equals”. As one combined entity, the two would have overtaken WPP as the largest agency holding group in the world – their market caps of roughly $14.5 billion (Publicis) and $16.5 billion (Omnicom) surpassing WPP’s $20 billion.

Thus, when the merger collapsed WPP was seen as a big winner. And the disarray and client uncertainty in the interim period worked further in the British group’s favour. Reuters reported that Publicis and Omnicom lost billions worth of business as a result of the confusion, which WPP agencies capitalised on by cutting fees to win new business.

As it turns out, neither company needed the merger to outsize their major rival. At the time of writing, Publicis’ market cap stands at €18.9 billion, roughly $20.65 billion. Omnicom’s meanwhile is $15.6 billion. WPP’s stands at £7.6 billion, or just under $9.5 billion.

The fall in WPP’s value is obviously notable. But so is the rise in Publicis’. As recently as 2020 it was the third largest of the holding groups, sitting behind both WPP and Omnicom.

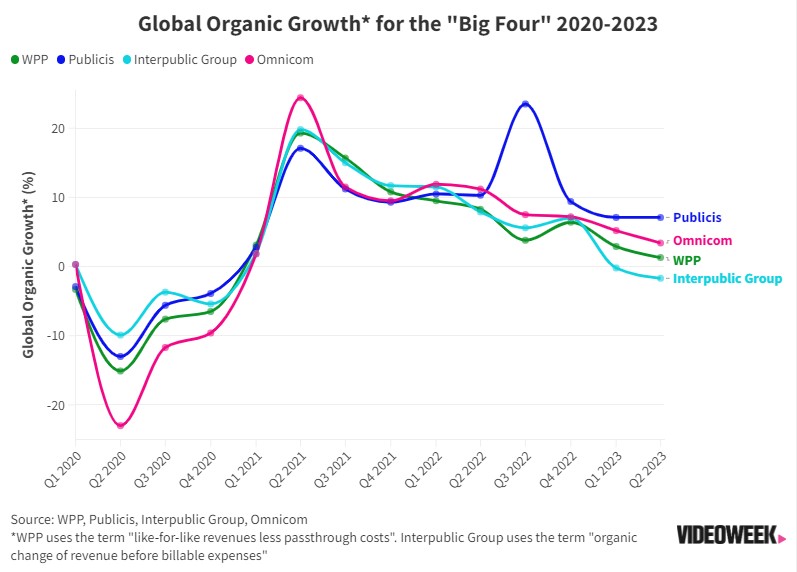

Now it’s the largest by a fair margin. This has been fuelled in part by Publicis’ recent performance: the agency has consistently posted organic growth and raised its guidance, at a time when competitors have had mixed results.

Market performance isn’t the only factor which influences a business’ valuation. But for Publicis, it’s been a major contributor. “The primary factor supporting their valuation growth is that Publicis has outperformed in terms of revenue growth and margin improvement, and its outlook has remained very strong,” said Brian Wieser, principal of Madison and Wall.

The question is, what exactly has fueled Publicis’ hot streak? The holding groups are often painted as fairly interchangeable – all built with the same basic principles in mind, and all facing the same challenges. What has Publicis been getting right?

Business balance

According to Publicis CEO Arthur Sadoun, the holding group’s hot streak comes down to two key factors. The first of these is Publicis’ “balanced revenue mix”, as he’s described it on multiple earnings calls.

Publicis’ revenues are now roughly equally split between three major segments: creative, media, and tech & data.

Media and creative are obviously the traditional domain of agency holding groups. While both are affected by clients’ decisions on how much to invest in advertising over any given period, they don’t move in exactly the same way. In recent quarters across agency groups, media revenues have tended to grow while creative has been stagnant or declining.

Publicis’ tech and data segment comprises revenues generated by Publicis Sapient and Epsilon. These units feed into media and creative, but they also bring in different types of work, such as digital business transformation contracts. And again, the factors which grow or shrink revenues here are a bit different to those which move media and creative. For example some businesses might dampen ad spend during tough economic climates if they feel that performance advertising isn’t going to generate much of a return, but may choose to invest in their own digital or data capabilities over the same period, eyeing up longer-term benefits.

Publicis isn’t unique in working across all these areas. And indeed in its recent Q3 results, Dentsu specifically pointed out larger business transformation projects as a weak point, with international clients putting these projects on hold.

But Sadoun says its equal split across media, creative, and data has positioned the group well to weather bumpy macroeconomic conditions. And this indeed seems to have played out in recent financial results. “Media and Sapient have been driving the growth,” says Madison and Wall’s Wieser – and these two segments have supported a leaner season for revenues from creative agencies.

Data a deciding factor

The second factor picked out by Sadoun is Publicis’ “unique go-to-market in media”. As mentioned above, Epsilon feeds into the media segment, powering large-scale personalisation of media.

“Every time we get into a pitch, we are leading what clients are looking for, which is personalisation at scale,” said Sadoun on Publicis’ most recent earnings call.

Competitors might raise their eyebrows at the idea that Publicis is unique in pairing up media with first-party data. All of the major holding group CEOs have been vocal about the importance of data for years.

But Epsilon, bought by Publicis for $4.4 billion in 2019, is a fairly unique asset. Other agency groups have similarly made major data acquisitions, such as IPG’s $2.3 billion purchase of Acxiom, and Dentsu’s acquisition of Merkle valued at around $1.5 billion for a majority stake. But Epsilon remains the biggest agency acquisition in the space.

“I don’t think any of the agencies necessarily do things radically different from one another, at least on the surface,” said Tim Nollen, senior media tech analyst at Macquarie. “The difference with Publicis may be that its Sapient and Epsilon acquisitions are serving it well, contributing to new business wins, and with their data capabilities helping it generate good returns on spending for clients.”

And it certainly seems to be helping Publicis win new business. R3’s new business ranking for 2022 found that Publicis won $331 million worth of new media business, double that of second placed WPP. Sadoun said on Publicis most recent earnings call that the group has “topped the new business rankings four times in the last five years and won over $10 billion in new media billings,” (though it’s not clear which new business ranking he was referring to).

And several major clients won by Publicis in recent years, including Disney, Novartis, and Walgreens, have cited Epsilon as a major factor.

Clients and markets

While Sadoun puts Publicis’ hot streak down to long term structural changes which have occurred within the business, a lot of Publicis’ growth compared with its rivals has happened over the past year. And it’s over this period where Publicis’ earnings have really stood out from its rivals. So it’s important to consider whether factors specific to this last year have played a significant role.

Looking at the figures, it looks like these short-term factors play a role, but don’t tell the full story.

For example a consistent theme over the past few quarters has been a pullback in advertising and marketing investment from tech and telecom clients. And it’s certainly true that Publicis is less reliant on revenues from these sectors than others. TMT (technology, media, and telecommunications) clients accounted for 12 percent of Publicis’ revenues in Q3. This is less than WPP for example, where tech clients alone make up 18 percent of revenues, and far less than S4 Capital, for whom tech clients contribute 43 percent of revenues.

But Publicis isn’t a massive outlier. Interpublic Group, which has cited the tech downturn as a major factor in recent drops in organic revenue, reported that tech clients contributed around 12 percent of revenues. While this is likely more than Publicis, since Publicis reported tech clients alongside telco and entertainment, it’s likely not a million miles off.

And we can see from results that Publicis saw a less steep drop from this client sector than others. In Q2, Publicis reported a three percent organic fall in tech revenues. Meanwhile WPP reported a 4.9 percent fall in revenues from tech and digital clients across H1. And IPG report that tech clients made up 12 percent of revenues in Q2 was down from 15 percent the previous year, suggesting a much steeper pullback in spending.

But these figures released by the agency groups may themselves be misleading. Ian Whittaker, founder of Liberty Sky Advisors, argues that the tech spending pullback – induced in large part by a sudden rise in US interest rates in 2022 which forced them to reduce costs – won’t solely appear within agency groups’ tech client listings.

For example, an ecommerce business might appear under ‘retail’. Or a fintech company could appear under ‘finance’. Thus, it’s possible that Publicis’ client base really has been much less weighted towards tech companies, in a way which is hard to read on financial statements.

Sometimes an individual agency group’s comparatively strong performance comes down to the markets where it’s strongest. For example, if an agency group is particularly strong in Europe, and European ad spend is comparatively strong over a few quarters, it’s not too surprising to see that agency group outperform its rivals.

At a glance, this doesn’t appear to be the case with Publicis. The French group has found growth in markets where others haven’t. In Q2. Publicis posted 4.9 percent organic growth in US revenues, while Omnicom posted 2.4 percent growth, and WPP and IPG both reported revenue drops.

Similarly in Europe, Publicis found 17 percent organic growth in Q2, much higher than any of its rivals (2.5 percent for Omnicom, 1.7 percent for IPG, and 9 percent for WPP across H1).

However, it’s also important to consider the types of business which each group runs in each market. Ian Whittaker pointed out that Publicis’ media business is particularly strong in the US, where media revenues across agencies have generally been higher. This therefore may have been a significant factor in Publicis’ recent results.

Swings and roundabouts

So Publicis’ recent success seems to be more than just a case of market factors working in the group’s favour.

But does that mean that Publicis is on a fundamentally different path from the other major holding companies? Not necessarily.

First, when looking at the growth in Publicis’ market cap, there have been factors at play beyond just market performance. Ian Whittaker says that the acquisitions of Sapient and Epsilon, while fuelling growth across the group, have also added major new units to Publicis’ business which inevitably increases its total value. WPP meanwhile has sold off the majority of Kantar, a major business unit, which will have had a shrinking effect on its market value.

And while Publicis is ahead of the curve at the moment, its strategy still doesn’t look fundamentally different from its competitors. All are fairly aligned on the need to break down barriers between the agencies they own, on the need to enable better use of data across the entire business, on the opportunities to work more holistically with clients beyond simply running and executing ad campaigns, and on the challenges and opportunities presented by AI.

As such, Publicis’ current run of success doesn’t necessarily mean it’s built an unbeatable advantage over its rivals. Rather, Publicis is currently seeing its investments and strategic moves pay off, buoyed by a few advantageous market factors. Others may see theirs similarly pay off further down the line.

“I think agency holding companies move in their own cycles,” said Macquarie’s Tim Nollen. “Publicis was in a rut a few years ago, now it appears to be running smoothly. All agency groups have their ups and downs that can last a few years; Publicis is on a relative up now.”